The £100k Illusion: Why Earning More in the UK Can Leave You With Less

Earning a six-figure salary feels like a major milestone, but for many in the UK, it comes with a hidden financial penalty. This is known as the £100k tax trap, where a pay rise can surprisingly leave you with less net income. It's caused by the tapering of your personal allowance, creating a punishing effective tax rate. This guide will explain exactly how this trap works, its impact on benefits like childcare, and the smart financial moves you can make, from salary sacrifice to pension contributions, to navigate it effectively.

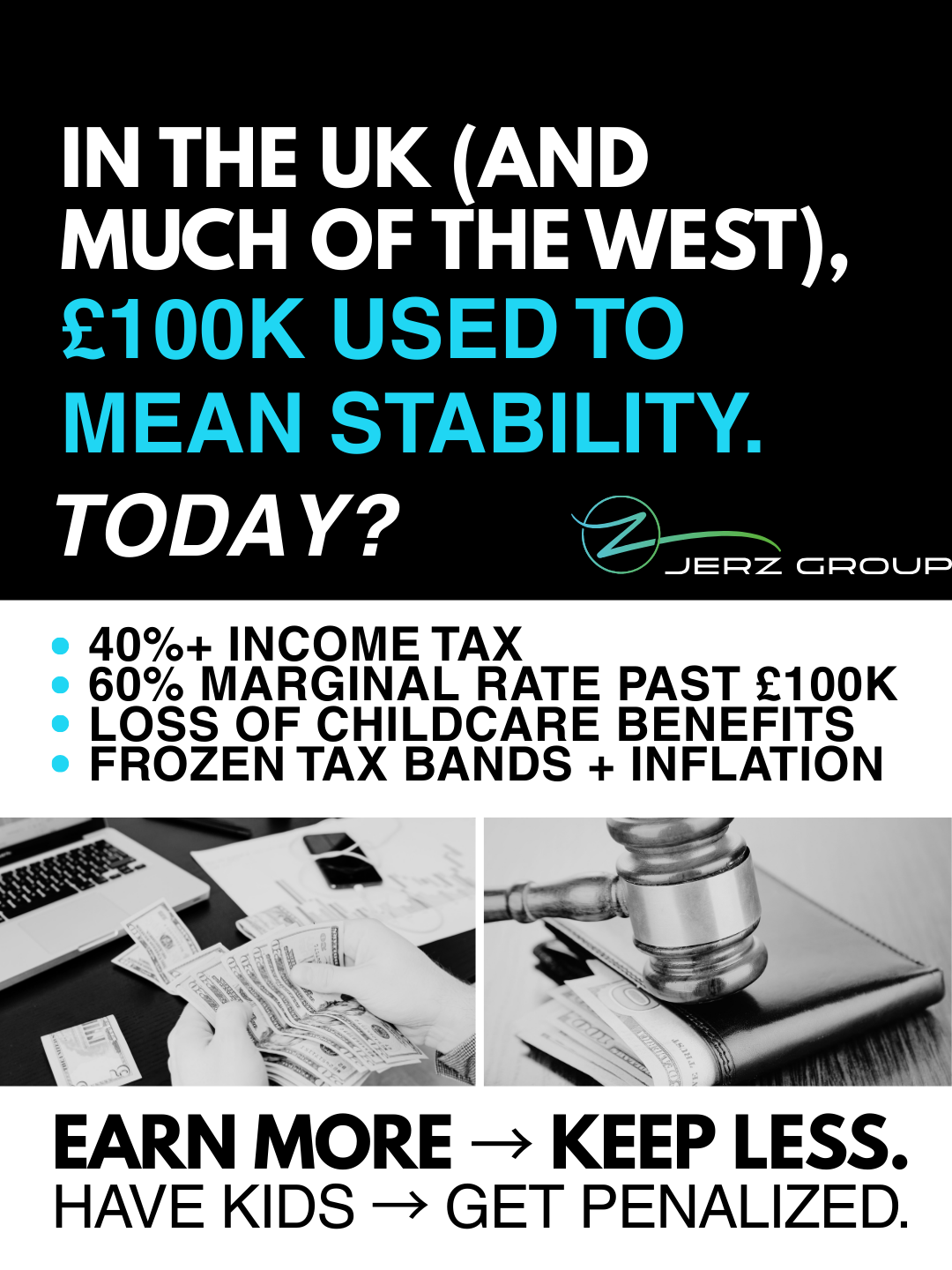

The Changing Meaning of a £100k Salary in the UK

Once considered the pinnacle of financial success, a £100,000 salary no longer guarantees the lavish lifestyle it once did. The rising cost of living and persistent inflation mean that this income doesn't stretch as far as it used to, changing the perception of what it means to be a high earner.

This shift creates a significant lifestyle gap between expectations and reality. As your effective tax rate increases, your net income is squeezed, leaving many to question if hitting the six-figure mark truly makes them "rich" in today's economy.

How Inflation and Rising Costs Alter Perceptions of Wealth

The value of money is constantly changing, and high inflation has significantly eroded the purchasing power of a six-figure salary. What £100,000 could buy a decade ago is vastly different from what it can cover today. Everyday expenses, from groceries and utility bills to fuel, have soared, eating into your net income.

This economic pressure means that even those with a substantial amount of income are feeling the pinch. The dream of financial security at this level is being challenged by the reality of escalating costs. More of your earnings are allocated to necessities, leaving less for savings, investments, or discretionary spending.

As a result, the definition of wealth is being recalibrated. A high salary on paper doesn't automatically translate to financial freedom when your net income is battling against a tide of rising prices, creating a lifestyle gap that many find surprising and difficult to manage.

The Lifestyle Gap: Expectations vs Reality on Six-Figure Incomes

Reaching a £100,000 income often comes with a set of lifestyle expectations: a larger home, comfortable savings, and financial peace of mind. However, the reality can be quite different, especially after taxes and essential costs are accounted for. The lifestyle gap is the void between the life you thought you'd have and the one your net income can actually afford.

This gap is widened by several factors that reduce your take-home pay. The loss of your personal allowance dramatically increases your effective tax rate, taking a larger chunk of your earnings than you might anticipate. Your individual circumstances, such as having a mortgage or dependents, further dictate where your money goes.

Key contributors to this lifestyle gap include:

- High housing costs, particularly in London and the South East.

- Significant childcare expenses, which can rival a second mortgage.

- The necessity of making substantial pension contributions for a comfortable retirement.

What is the £100k Tax Trap in UK?

The £100k tax trap is a term for a quirk in the UK tax system that creates an unusually high effective tax rate for people earning just over £100,000. It's not an official tax band but a consequence of how your tax-free personal allowance is withdrawn once your income crosses this threshold.

Essentially, for every £2 you earn over £100,000, you lose £1 of your personal allowance. This tapering continues until your allowance disappears completely at an income of £125,140. This creates a financial cliff edge that many are unprepared for in the tax year their income increases.

Personal Allowance Taper Explained

Every taxpayer in the UK is entitled to a personal allowance, which is a set amount of income you can earn without paying any tax. For the current tax year, this amount is £12,570. However, this benefit starts to diminish once your adjusted net income exceeds £100,000.

The rule for the tapering of the personal allowance is straightforward: your allowance is reduced by £1 for every £2 you earn above the £100,000 threshold. This means that income in this bracket is hit twice. It's taxed at the higher income tax rate, and it also causes a portion of your previously tax-free income to become taxable.

Here’s how it works:

- If you earn £102,000, your personal allowance is reduced by £1,000.

- If you earn £110,000, your allowance is reduced by £5,000.

- Once your income reaches £125,140, your entire personal allowance of £12,570 is gone.

This reduction must be accounted for on your tax return and is a primary reason for the punishing 60% effective tax rate.

The 60% Tax Rate UK: How Does It Happen?

The alarming 60% tax rate isn't an official rate set by HMRC but an effective rate caused by the personal allowance taper. When you earn between £100,000 and £125,140, you face a double hit: you pay the 40% higher rate of income tax on your earnings, and you also pay 40% tax on the personal allowance you lose.

Let's break it down. For every £100 you earn over £100,000, you immediately pay £40 in income tax. In addition, you lose £50 of your personal allowance. This lost allowance was previously tax-free, but it is now taxed at 40%, adding another £20 to your tax bill (£50 x 40%). In total, you pay £60 in tax on that £100 of income, creating an effective 60% tax rate.

This table illustrates the impact as your income grows:

This demonstrates how quickly the tax trap can diminish your net income.

Why Does the 60% Marginal Tax Rate Exist at £100,000?

The 60% marginal tax rate isn't a deliberate policy to tax people at that specific figure. Instead, it's a consequence of the mechanism used to withdraw the personal allowance from high earners. The government introduced the tapering of the personal allowance as a way to raise revenue from those with higher incomes without changing the main income tax rates.

This approach creates a 'cliff edge' where the effective tax rate spikes sharply. The policy is designed to ensure that the benefit of the tax-free allowance is gradually removed, making the tax system more progressive. However, its implementation results in the confusing and punitive 60% marginal rate of tax for earnings within a specific band.

UK Marginal Tax Rate 100k: How the Numbers Work

Understanding the marginal tax rate 100k is about seeing how each extra pound you earn is taxed. When your income is between £100,000 and £125,140, the combination of the 40% higher income tax rate and the loss of your personal allowance creates this punishing effective tax rate.

For every additional £2 you earn in this bracket, you not only pay 80p in income tax (40% of £2) but also lose £1 of your tax-free personal allowance. This £1 of lost allowance is now subject to tax at 40%, costing you an extra 40p. So, for that £2 extra earning, your total tax increases by £1.20 (80p + 40p). This equates to a 60% tax rate on that income.

Let's simplify the maths on a £1,000 pay rise over £100k:

- You pay £400 (40%) in standard income tax on the £1,000.

- You lose £500 of your personal allowance.

- This lost allowance is now taxed at 40%, costing you an extra £200.

- Your total tax on the £1,000 rise is £600, which is a 60% effective tax rate.

This calculation doesn't even include National Insurance, which adds another 2% tax, pushing the real marginal rate to 62%.

Simple Example: Earning Just Over the Threshold

Imagine you receive a £1,000 bonus, taking your total income from £100,000 to £101,000 for the tax year. At first glance, this seems like great news. However, this small pay rise triggers the tax trap, significantly reducing your net income gain.

Because you've crossed the threshold, you instantly lose £500 of your personal allowance. This means £500 of your income that was previously tax-free is now taxed at 40%, creating an extra tax charge of £200. On top of that, the £1,000 bonus itself is taxed at 40%, which is another £400.

The outcome of this £1,000 pay rise is:

- Original income: £100,000

- New income: £101,000

- Total extra tax paid: £600 (£400 + £200)

- Actual take-home from the £1,000 bonus: Just £400.

This is a clear illustration of how the tax trap can make a pay rise far less rewarding than you would expect, which is why strategies like salary sacrifice are so important.

The Childcare Cliff Edge: Financial Penalties Above £100k

Beyond the direct tax implications, crossing the £100,000 income threshold creates another significant financial obstacle for parents: the childcare cliff edge. Once your adjusted net income for the tax year goes even £1 over this limit, you lose eligibility for two major government childcare support schemes.

This includes losing access to Tax-Free Childcare and the extended hours of free childcare. For families with young children, the value of these benefits can be thousands of pounds per year. A seemingly positive pay rise can inadvertently trigger a substantial financial loss, making family finances more challenging.

Childcare Income Limit and What You Lose

The childcare income limit is set at an adjusted net income of £100,000 per parent. If you or your partner earn above this, your family becomes ineligible for crucial support, creating a harsh financial cliff edge. It doesn't matter if the other parent earns much less; if one exceeds the limit, the benefits are lost for the entire family.

The two main schemes you lose access to are Tax-Free Childcare, which provides up to £2,000 per child per year towards childcare costs, and the 30 hours of free childcare for three and four-year-olds in England. For families with multiple young children, the combined loss can be substantial.

Here’s what you stand to lose:

- Tax-Free Childcare: The government contributes £2 for every £8 you pay for childcare, up to £2,000 per child annually.

- 30 Hours Free Childcare: This benefit, which is an extension of the universal 15 hours, can save families thousands of pounds a year on nursery or childminder fees.

Losing these benefits can have a greater financial impact than the tax increase from the personal allowance taper alone, dramatically increasing the effective rate of tax on your pay rise.

Real-Life Scenario: When a Pay Rise Reduces Take-Home Pay

Consider a parent earning £99,000 a year whose family benefits from Tax-Free Childcare, saving them £2,000 annually. They receive a £2,000 pay rise, bringing their income to £101,000. While this seems like a positive step, the financial consequences are severe.

This small pay rise pushes them over the £100,000 threshold. Not only do they fall into the 60% tax trap on that extra income, but they also lose the £2,000 childcare support. The tax on the pay rise and the lost benefits combined can leave them financially worse off than they were before the promotion.

Here's the breakdown:

- A £2,000 pay rise to £101,000 triggers an extra tax bill of £600 due to the tax trap.

- The family loses their £2,000 Tax-Free Childcare benefit.

- The net effect is a financial loss of £600, despite earning more.

This scenario highlights why seeking financial advice is crucial when your income approaches this level, as a pay rise can unintentionally reduce your overall net income. It's essential to check your tax return carefully in these situations.

Fiscal Drag and Frozen Tax Bands: The Silent Squeeze

The £100k tax trap is made worse by a wider economic issue known as fiscal drag. This happens when tax thresholds, like the personal allowance and income tax bands, are frozen instead of rising with inflation. As wages increase to keep up with the cost of living, more people are pushed into higher tax brackets.

This phenomenon acts as a "stealth tax" because the government collects more tax revenue without explicitly raising tax rates. Frozen tax bands mean your pay rises are taxed more heavily, reducing your real-term net income and quietly increasing your effective tax rate over time.

What Are Frozen Tax Bands and Why They Matter

Frozen tax bands refer to the government's decision not to increase income tax thresholds in line with inflation. Typically, these bands would rise each year, meaning you could earn a bit more before paying a higher rate of tax. However, when they are frozen, even a modest, inflation-matching pay rise can push you into a higher tax bracket.

This matters because it silently increases the tax burden on workers. The £100,000 threshold for the personal allowance taper has not changed for years, meaning fiscal drag is pulling more and more people into the 60% tax trap. It's a key reason why the number of people affected by this trap has surged.

The consequences of frozen tax bands include:

- More people paying the 40% higher rate of tax for the first time.

- An increasing number of earners being caught in the 60% tax trap.

- A higher overall tax burden on the workforce, which feels like a stealth tax.

This policy effectively means you are paying more tax without any change in the headline tax rates.

How Fiscal Drag Quietly Raises Your Taxes

Fiscal drag works subtly to increase your tax bill over time. When your salary increases to keep pace with inflation, your purchasing power should theoretically stay the same. However, with frozen income tax bands, that pay rise can push you across a tax threshold, such as the £100,000 limit where the personal allowance begins to taper.

This means a larger portion of your income is taxed at a higher rate. For example, a salary that was comfortably below the higher-rate threshold five years ago might now be well within it, even if your real-terms pay hasn't actually increased. Your effective tax rate goes up, and your net income shrinks relative to the cost of living.

The effects of fiscal drag are clear:

- It pulls thousands more people into the 60% tax trap each tax year.

- It erodes the value of pay rises, diminishing the incentive to earn more.

- It acts as a stealth tax, allowing the government to collect more revenue without announcing official tax hikes.

This silent squeeze makes proactive tax planning more important than ever for managing your finances.

The Wider Impact: How Tax Codes Shape Financial Choices

Tax codes are more than just a mechanism for collecting revenue; they create powerful incentives that shape people's financial and life choices. The existence of a 60% effective tax rate at the £100,000 threshold actively discourages earning more within that specific income bracket, leading to some surprising behaviors.

Faced with such a high marginal tax rate, individuals often adjust their work patterns, investment decisions, and even family planning. A financial adviser can help navigate these complex choices, which often depend on individual circumstances and the specific tax treatment of different income sources.

Turning Down Promotions or Restructuring Income

It may sound counterintuitive, but the £100k tax trap UK leads some professionals to turn down promotions or pay rises. When a salary increase pushes you into the 60% tax zone and causes you to lose childcare benefits, the net financial gain can be minimal or even negative. The promotion penalty becomes a real deterrent to career progression.

Instead of accepting a higher salary, some individuals negotiate for other benefits, such as more holiday time, a better work-life balance, or increased employer pension contributions. Others might choose to reduce their working hours or transition to part-time work to keep their net income below the £100,000 threshold.

Common responses to the tax trap include:

- Requesting to cap salary at £100,000 and receive the excess as a future bonus.

- Negotiating a salary sacrifice arrangement for non-cash benefits.

- Actively choosing not to pursue roles that would tip their income over the edge.

These decisions are rational responses to a tax system that heavily penalizes earning more at a specific income level.

Couples Adjusting Work and Family Plans Due to Tax Pressures

The tax trap doesn't just affect individuals; it influences how couples structure their work and family lives. When one partner's income approaches £100,000, families must make strategic decisions to avoid losing thousands of pounds in tax and benefits, particularly free childcare.

This can lead to one partner deliberately limiting their earnings or hours to keep the household's finances optimized. For instance, a couple might decide that it is more beneficial for one person to stay under the threshold, even if it means sacrificing career advancement. A financial adviser can be invaluable in helping couples model these scenarios.

These adjustments can manifest in several ways:

- One partner taking on more unpaid domestic responsibilities to allow the other to maximize their career without tipping the family into the trap.

- Structuring self-employed income or business dividends to be split more evenly between partners.

- Delaying having children or spacing them out to avoid the highest childcare cost years coinciding with peak earning years.

These are significant life decisions driven by pressures in the tax code.

Is £100,000 Still “Rich” in the United Kingdom?

The question of whether a £100,000 salary makes you "rich" in the UK is more complex than ever. While it's undoubtedly a high income, the lifestyle it affords has been significantly eroded by a high effective tax rate, the loss of the personal allowance, and soaring living costs.

After taxes, mortgage payments, childcare, and pension savings, the remaining net income can feel surprisingly average, particularly in expensive parts of the country. This creates a major lifestyle gap, forcing many to question the traditional definition of wealth and what it takes to be financially secure today.

High-Income Life in London vs Other UK Regions

Your perception of a £100,000 salary is heavily influenced by where you live. In London and the South East, where housing costs are exceptionally high, a six-figure income can feel distinctly middle-class. A significant portion of your net income is immediately consumed by mortgage or rent payments, which can be double or triple the amount paid in other regions.

In contrast, earning £100,000 in parts of Northern England, Scotland, or Northern Ireland can afford a much more comfortable lifestyle. Lower property prices and general living costs mean your net income stretches considerably further, allowing for more savings, investments, and discretionary spending.

The regional differences are stark:

- Housing: The average house price in London is more than double that of many other UK regions.

- Commuting: Transport costs into major city centers can eat up a large slice of monthly income.

- Overall Costs: Everything from socialising to services tends to be more expensive in the capital.

This disparity in the amount of income needed for a similar quality of life highlights that a salary figure alone is not a true measure of wealth.

Big Expenses: Mortgages, Childcare, and Pension Saving

For many high earners, a large portion of their income is already committed to major life expenses before they even think about discretionary spending. These "big three" costs (mortgages, childcare, and pensions) can consume the majority of a household's net income.

Childcare costs in the UK are among the highest in the world. For families with young children, this expense alone can be equivalent to a second mortgage payment, making the loss of free childcare support over the £100k threshold particularly painful. Similarly, high property prices mean that mortgage payments take a substantial bite out of monthly earnings.

Essential financial commitments include:

- Mortgage/Rent: Often the largest single monthly outgoing.

- Childcare Costs: Can exceed £1,000-£1,500 per month per child.

- Pension Saving: Financial experts recommend saving 15% or more of your salary for a comfortable retirement, a significant and necessary deduction from your take-home pay.

When these are factored in, the remaining disposable income on a £100,000 salary can feel surprisingly modest.

Should You Stay or Go? Geographic Options for High Earners

The combination of high taxes and the rising cost of living is prompting a growing number of high earners to consider their geographic options. With the rise of remote work, professionals are no longer tied to expensive cities. This newfound global mobility allows them to explore living in places with a more favorable tax geography.

This isn't about evading tax but making strategic decisions about where to live and work to maximize net income and quality of life. The question is no longer just about finding a better job, but finding a better place to build a life, whether that's a different UK region or another country entirely.

Remote Work, Global Mobility, and “Tax Geography”

The normalisation of remote work has fundamentally changed the career landscape. Professionals in many fields can now perform their roles from anywhere, opening up the possibility of "tax geography," the practice of choosing a location to live based on its tax system and cost of living. This gives individuals unprecedented control over their net income.

This global mobility allows high earners to escape the financial squeeze of high-tax, high-cost areas. Why live in an expensive city with punishing tax rates when you can do the same job from a location with a lower cost of living and a more favorable tax regime? It's a rational choice based on optimising your financial circumstances.

This trend is creating new possibilities:

- Becoming a "digital nomad" and working from countries with lower income taxes.

- Relocating to financial hubs like Dubai, Panama, Paraguay or Singapore that offer zero or low income tax.

This strategic relocation is becoming a key part of financial planning for a mobile workforce.

Follow Jerz