Key Highlights

Here are the key takeaways from our guide on financial structure:

- A company's financial structure is the specific mix of debt and equity used to fund its operations, as shown on its balance sheet.

- The main components are debt financing (loans, bonds) and equity financing (owner's capital, retained earnings).

- A balanced structure is essential for managing financial risk and ensuring long-term stability.

- Your choice between debt and equity directly impacts the ownership of the company and overall control.

- Factors like your industry, company goals, and risk appetite influence the ideal financial structure for your business.

Introduction

Imagine planning a long road trip. You wouldn't just jump in the car; you'd think about the right vehicle and how much fuel you need. Similarly, your business needs the right fuel—money—to run smoothly. This is where your financial structure comes into play. It’s the mix of borrowed funds and owner's capital that powers your company. Understanding your company's financial structure, which is detailed on the balance sheet, is crucial for navigating risks, fueling growth, and reaching your destination successfully.

Defining Financial Structure in Simple Terms

What does financial structure mean in simple terms? It’s the way your company organizes its finances by combining different sources of funds. Think of it as the recipe for how you pay for everything, from day-to-day operations to big expansion projects. This mix is shown on the right side of your balance sheet.

While people often confuse it with capital structure, financial structure is the broader term. It includes all of your liabilities—both short-term and long-term—whereas capital structure only looks at long-term debt and equity.

Key Concepts of Financial Structure for Canadian Businesses

For any business, including those in Canada, the financial structure is built on a few core ideas. The two primary ways to fund your company are through debt financing and equity financing. Debt involves borrowing money that you must pay back with interest, while equity means selling an ownership stake in your business.

The choice between these two affects your cost of capital—the price you pay for using someone else’s money. Debt is often cheaper, but it comes with fixed repayment obligations. Equity doesn't require repayment, but it dilutes the owner's control over the business.

Ultimately, the goal is to find the right balance. A healthy mix ensures you can fund your operations and growth without taking on too much risk. This balance influences your company’s profits and its ability to generate value for shareholders over the long term.

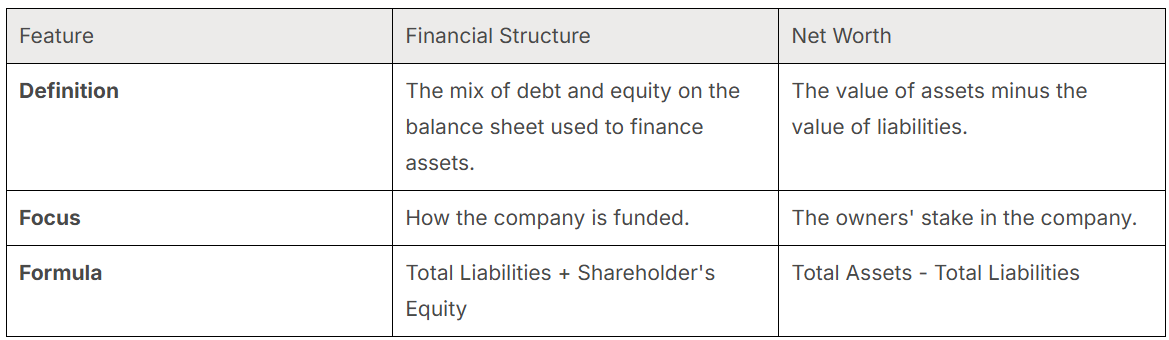

Differences Between Financial Structure and Net Worth

It's easy to mix up financial structure and net worth, but they represent different aspects of your company's finances. Your financial structure is the combination of all liabilities and equity used to fund your assets. It’s about how your business is capitalized.

In contrast, net worth (or shareholder's equity) is what’s left after you subtract all liabilities from your assets. It represents the value belonging to the owners. While related, financial structure is a broader picture of funding, and net worth is a component within that picture. The equity ratio, a part of financial analysis, helps show this relationship.

Here’s a simple table to highlight the differences:

Role of Invisible Assets and Asset Invisibility

How do invisible assets factor into a company's financial structure? While a balance sheet clearly lists physical and financial assets, some of a company's most valuable resources are intangible. These "invisible assets" can include your brand reputation, proprietary processes, and the strength of your management team.

These elements don't have a line item, but they significantly impact your ability to secure funding. Strong invisible assets can boost investor confidence, making it easier to raise equity or secure favorable loan terms. Their value is reflected in the company's performance and growth potential, which funders carefully assess.

Therefore, asset invisibility doesn't mean a lack of value. When investors decide to take an ownership stake, they are betting on these intangibles just as much as the physical assets. A company's ability to create value is tied to these unseen strengths, which are a crucial, if unstated, part of its overall financial foundation.

Core Components of Financial Structure

What are the main components of a financial structure? At its core, a company’s financial structure is built from two primary sources of capital: debt and equity. These components are how a business gathers the funds needed to operate, invest, and grow.

Understanding each one is key to building a healthy financial foundation. Below, we'll explore equity capital and its ties to ownership, debt capital and its associated obligations, and the importance of working capital management for daily operations.

Equity Capital and Ownership Dynamics

Equity capital is the money invested in the business by its owners, often called owner’s capital. This can come from the initial funds used to start the company (share capital) or from profits that are reinvested back into the business (retained earnings). Unlike a loan, this money doesn't need to be repaid.

The trade-off for this flexibility is a dilution of ownership. When you bring in new investors, you are selling them an ownership stake in your company. This means they get a claim on future profits and a say in how the business is run.

Your goal is to use equity to grow the business and increase shareholder value. While it reduces your personal control, successful equity financing can provide the fuel for significant expansion and long-term success, ultimately making everyone's ownership of the company more valuable.

Debt Capital and Credit Arrangements

Debt capital refers to funds your company borrows and must pay back over time, usually with interest. Common sources include loans from financial institutions or the issuance of bonds to investors. This is a popular way to get quick access to funds for specific projects or operational needs.

The key feature of debt is the financial obligation it creates. You must make regular payments, including interest, regardless of your company's profitability. The interest rate on your debt is a critical factor, as it determines the total cost of borrowing.

While taking on debt increases financial risk, it allows you to retain full ownership of your company. As long as you meet your repayment obligations, lenders have no say in your business decisions. It’s a powerful tool for growth if managed responsibly.

Working Capital Management Strategies

Beyond long-term funding, effective working capital management is vital for day-to-day stability. This involves managing your short-term assets (like cash and inventory) and short-term liabilities (like accounts payable) to ensure you always have enough liquidity to cover immediate expenses.

Proper management ensures your cash flows are smooth and prevents financial stress. It helps you avoid a situation where you can't pay your bills, even if your company is profitable on paper. Retained earnings often play a crucial role in providing a buffer for working capital.

Effective strategies include:

- Optimizing inventory levels to avoid tying up too much cash.

- Managing accounts receivable to get paid by customers faster.

- Negotiating favorable payment terms with suppliers.

- Exploring short-term financing options when needed.

Importance of Financial Structure for Business Stability

Why is financial structure important for businesses? A solid financial structure is the backbone of your company's financial health and stability. It's not just about having money; it's about having the right kind of money. A balanced financial structure allows your business to weather economic storms, seize growth opportunities, and operate efficiently.

An imbalanced structure, such as one with too much debt, can create significant risk and limit your options. Let's look at how your choices impact risk management, investor confidence, and the long-term control of your business.

How Financial Structure Impacts Risk Management

How does a company's financial structure affect its stability? Your financial structure is a key determinant of your company's financial risk. A business that relies heavily on debt financing faces higher risk because it has fixed debt obligations that must be met, no matter what. If revenues decline, these payments can become a heavy burden.

Effective risk management involves finding the right balance within your capital structure. By incorporating equity, which doesn't require repayment, you lower your financial risk and build a more resilient company. This buffer can be the difference between surviving a downturn and facing insolvency.

Ultimately, every business must decide on its risk tolerance. While debt can amplify returns in good times, a more balanced structure provides stability and a safety net when unexpected challenges arise, making it a cornerstone of prudent financial planning.

Influence on Flexibility, Growth, and Investor Confidence

A well-planned financial structure gives your company the flexibility to adapt and grow. With access to different financing options, you can respond quickly to changing market conditions. For example, you might use debt for a predictable expansion or seek equity to fund a bold new venture.

This adaptability directly fuels growth. Without a reliable way to fund new projects, hire talent, or enter new markets, your business can stagnate. A strong financial structure ensures you have the resources ready when opportunity knocks.

Moreover, it builds investor confidence. Investors and lenders look for companies that manage their finances prudently. A balanced structure signals that you are not overly reliant on debt and have a solid plan for the future, making them more willing to provide the capital you need to succeed.

Control, Ownership, and Business Longevity

The decisions you make about your financial structure have a lasting impact on the ownership of the company. When you choose equity financing, you are selling a piece of your business. This dilutes your control but can provide the capital needed for rapid growth and greater business longevity.

On the other hand, debt financing allows you to retain full ownership and control. You are the one calling the shots, as long as you meet your repayment obligations. However, too much debt can restrict your ability to pursue long-term strategic goals if cash flow is tight.

Finding the right balance is about aligning your financing strategy with your vision. Do you want to grow as fast as possible, even if it means sharing control? Or is maintaining full ownership your top priority? The answers will shape your company's future for years to come.

Factors Influencing the Optimal Financial Structure

There's no one-size-fits-all formula for the perfect financial structure. The optimal financial structure for your business depends on a unique blend of internal and external factors. You need to consider everything from your industry and company goals to your team's capabilities and your appetite for risk.

Achieving the right balance between your capital ratio and cost of capital requires careful thought. Let's examine some of the key elements that financial leaders consider, including industry benchmarks, your company's lifecycle stage, and your management team's risk profile.

The Effect of Industry, Company Lifecycle, and the Global System

Your industry plays a huge role in defining a suitable financial structure. For instance, a software company with stable, recurring revenue might comfortably take on more debt than a construction firm with cyclical cash flows. Industry benchmarks provide a good starting point for what’s considered normal.

The company lifecycle is another critical factor. An early-stage startup in hyper-growth mode will likely need equity financing to hire talent and build its product. In contrast, a mature, stable company might prefer debt financing for predictable expansions, as its cash flows can easily cover the payments.

Finally, the broader global system, including economic trends and regulations, can influence your choices. The financial services industry, for example, is heavily regulated, which dictates how firms can be capitalized. Being aware of these external forces is crucial for making smart financing decisions.

Risk Appetite, Management Capabilities, and Company Evolution

Your company’s risk appetite is a fundamental driver of its financial structure. Are you willing to take on significant debt for the chance of higher returns, or do you prefer the lower-risk path of equity, even if it means slower growth? This decision reflects the core philosophy of your leadership team.

The capabilities of your financial management team are also key. A sophisticated team can manage complex debt instruments and relationships with investors, opening up more financing options. Without that expertise, a simpler structure may be more appropriate for the company's evolution.

A sound financial structure is dynamic and adapts as your business changes. Key considerations include:

- The personal goals of the founders (e.g., lifestyle business vs. rapid exit).

- The strength and experience of the management team.

- The company's historical performance and future projections.

Public versus Private Enterprises and Residency Considerations

The ideal financial mix differs significantly between public and private companies. Public companies, by definition, have access to capital markets through public offerings of their stock. However, they are also subject to market fluctuations, shareholder expectations, and strict reporting requirements.

Private companies typically have more flexibility. They are not beholden to Wall Street analysts or the daily ups and downs of the stock market. This allows owners to make decisions, such as taking on new investors or debt, without needing to satisfy a broad range of outside constituents beyond their board and shareholders.

While not always a primary factor, residency can also play a role, especially for companies operating across borders. Tax laws, regulations, and access to capital can vary by location, influencing decisions around initial public offerings or seeking private funding in different jurisdictions.

Tax Planning and Tax-Aware Structuring

What role does tax planning play in financial structuring? Your financial structure isn't just about funding; it's also a powerful tool for tax planning. The choices you make between debt and equity can have significant tax implications. For example, interest payments on debt are often tax-deductible, which can lower your overall tax bill.

Effective tax-aware structuring involves designing your finances to be as efficient as possible under the current tax policy. This proactive approach can save your company a substantial amount of money, freeing up cash for reinvestment and growth.

Essentials of Tax-Aware Financial Structuring in Canada

For businesses operating in Canada, tax-aware financial structuring is a critical part of financial planning. The goal is to align your financing options with Canadian tax laws to minimize your obligations legally. Different tax rates on capital gains versus regular income, for example, can influence whether you favor equity or debt.

A key consideration is the tax-deductibility of interest payments on debt, which can make it an attractive option. However, this must be balanced against the risks. A structure that saves on taxes but makes the company financially unstable is not a winning strategy.

When designing your structure, keep these points in mind:

- Consult with a tax professional who understands the specifics of Canadian corporate tax law.

- Consider how different sources of income and financing are treated under current tax policies.

- Structure your finances to support your long-term goals, not just short-term tax savings.

Incorporating Residency and Global System Factors in Tax Strategy

As a business expands, its tax strategy must evolve to account for global factors. A company's residency, and the residency of its owners, can determine which country's tax laws apply. Operating in multiple jurisdictions adds layers of complexity, requiring careful planning to ensure compliance and efficiency.

The global system of international tax treaties and regulations also plays a crucial role. These agreements can prevent double taxation but also create reporting obligations. Your financial management team needs to stay informed about changes in international tax policy that could impact your business.

Ultimately, an effective global tax strategy integrates these external variables. It ensures that your financial structure is not only sound from an operational perspective but also optimized for the international environment in which you do business.

Unique Financial Structures for Small Businesses and Specialized Groups

Can you provide examples of financial structures for small businesses? The textbook financial structure doesn't always apply to everyone. Small businesses, startups, and other specialized groups often have unique needs and access to different financing options. Their structures are typically designed for flexibility and to support growth in the early stages.

These groups must be creative in how they secure funding. Their financial journey might involve a mix of personal savings, loans from friends and family, and eventually, more formal sources of capital. Let's explore some common examples for these unique entities.

Examples for Small Businesses and Startups

The financial structure of startups and small businesses often evolves as they grow. In the very beginning, the primary sources of capital might be the founders' own savings, along with loans from family and friends. This initial funding is crucial for getting the business off the ground.

As the business develops a track record, it may gain access to more traditional financing. This could include small business loans from banks or credit unions. For high-growth startups, seeking equity from angel investors or venture capitalists is a common path to secure the large amounts of capital needed for scaling.

Common early-stage financing sources include:

- Personal funds and "friends and family" rounds.

- Small business loans and lines of credit.

- Venture capital for startups with high growth potential.

Approaches for Expats, Digital Nomads, and Dynastic Wealth

Specialized groups like expats and digital nomads face unique financial challenges. Operating within a global system, they need a financial structure that is flexible and portable. Their planning often involves managing assets and income across multiple currencies and tax jurisdictions, requiring a sophisticated approach to maintain a stable financial position.

For individuals and families with dynastic wealth, the focus is on preservation and multi-generational growth. Their financial structures are designed for the long term, often incorporating trusts and other legal entities to protect assets and ensure a smooth transfer of wealth to future generations.

In each case, the financial structure is tailored to the group's specific circumstances. For expats, it's about navigating international complexity. For the wealthy, it's about longevity and legacy. Both require careful, strategic planning far beyond a simple debt-equity mix.

The Role of Dynastic Wealth in Financial Structure

How is dynastic wealth related to financial structure? Dynastic wealth refers to significant fortunes passed down through multiple generations. Its relationship with financial structure is centered on long-term preservation and growth. The goal is not just to fund a business for a few years but to create a legacy that lasts for decades or even centuries.

This long-term perspective requires sophisticated structures that go beyond a typical corporate setup. Strategies often involve family offices, trusts, and detailed succession models to manage the wealth, minimize taxes, and ensure a smooth transition of control and assets over time.

Building Multi-Generational Growth through Strategic Planning

For families with dynastic wealth, strategic planning is the key to achieving multi-generational growth. This process involves creating a financial structure that is resilient enough to withstand market cycles, tax law changes, and evolving family dynamics over many decades.

The focus is on sustainable growth rather than high-risk, short-term gains. Investments are often diversified across various asset classes, and businesses owned by the family are capitalized in a way that prioritizes stability and longevity. The financial structure is designed to produce steady returns while protecting the principal capital.

By aligning the family's long-term vision with a robust and flexible financial plan, dynastic wealth can continue to grow and support future generations. This forward-looking approach is the essence of building a lasting financial legacy.

Integrating Family Offices, Trusts, and Succession Models

To manage dynastic wealth effectively, families often use specialized tools within their financial structure. Family offices, which are private wealth management firms that serve a single family, are a common vehicle for overseeing complex financial affairs.

Trusts are another essential component. They are legal arrangements that allow a third party (the trustee) to hold and manage assets on behalf of beneficiaries. This helps protect assets from creditors, ensures they are managed professionally, and facilitates the transfer of wealth according to the family's wishes.

Key elements for managing dynastic wealth include:

- Family Offices: Centralize financial management, investment strategy, and tax planning.

- Trusts: Provide asset protection and a clear framework for wealth transfer.

- Succession Models: Create a clear plan for passing leadership and ownership to the next generation.

How Globalization Shapes Financial Structure

Does globalization impact the financial structure of companies? Absolutely. In today's interconnected world, globalization has a profound effect on how companies fund themselves. Businesses can now access international markets for capital, opening up a wider range of financing options than ever before. This allows them to seek funding where conditions are most favorable.

However, operating on a global scale also introduces new complexities. Companies must navigate different currencies, interest rates, and regulatory environments. This requires making cross-border adjustments to the financial structure to manage new risks and opportunities effectively.

Effects of International Markets, Currencies, and Cross-Border Adjustments

Access to international markets gives companies more choices for raising capital. A business might issue bonds in Europe to take advantage of lower interest rates or list on a foreign stock exchange to attract a new class of investors. This flexibility can lead to a lower cost of capital and a more diversified funding base.

However, this comes with challenges. Fluctuations in currencies can dramatically affect the value of foreign-denominated debt and revenue. A sudden drop in a foreign currency could increase a company's debt burden in its home currency overnight. Financial institutions offer hedging tools to manage this risk.

Managing a global financial structure involves:

- Monitoring foreign exchange rates and using strategies to mitigate currency risk.

- Complying with the regulations of different countries where capital is raised.

- Making cross-border adjustments to optimize the company’s global tax position.

Managing Global System Risks for Canadian Companies

For Canadian companies operating internationally, managing global system risks is essential. These risks go beyond simple market fluctuations and include political instability, changes in international trade policies, and global economic downturns. These events can disrupt supply chains, impact consumer demand, and affect access to capital.

A company's risk profile must account for these external threats. A business with significant operations abroad might choose a more conservative financial structure, with lower debt levels, to provide a cushion against unforeseen global shocks.

Effective management involves continuous monitoring of the global landscape and creating a financial structure that is resilient enough to handle uncertainty. By planning for potential financial risk from the global system, Canadian companies can better protect their operations and maintain stability in a volatile world.

Case Studies: Financial Structure in Practice

Theory is one thing, but seeing financial structure in practice brings these concepts to life. By looking at practical examples and case studies, you can better understand how different companies find their ideal balance of debt and equity. It highlights how a well-managed structure contributes to financial health and success.

These real-world scenarios show that there is no single right answer. The best structure is one that aligns with a company's specific goals, industry, and circumstances. Let's explore some success stories and lessons learned.

Canadian Business Success Stories

Consider a hypothetical Canadian tech company that started with equity from angel investors. This allowed it to fund research and development without the pressure of debt repayments. The financial structure was light on debt, which was appropriate for its high-risk, high-growth phase.

As the company matured and generated predictable revenue, its leaders strategically took on debt to fund expansion into new markets. They adjusted their balance sheet to reflect their new, more stable position. This allowed them to finance growth without further diluting ownership.

This Canadian business success story illustrates the importance of an evolving financial structure. By adapting their financing strategy to match their lifecycle stage and tolerance for market changes, they were able to scale successfully while maintaining strong financial health.

Lessons from Expats and Digital Nomads

The experiences of expats and digital nomads offer valuable lessons in financial flexibility. Imagine a freelance consultant working for clients across several countries. Their income arrives in different currencies, and their expenses are spread across multiple jurisdictions. A rigid financial structure would be impractical.

The key lesson is the need for a dynamic and adaptable financial plan. These individuals often use multi-currency bank accounts, rely on fintech solutions for low-cost transfers, and maintain a clear picture of their global assets and liabilities. They prioritize liquidity and flexibility over complex, long-term debt arrangements.

Their financial structure is designed to handle uncertainty and constant change. By embracing cross-border adjustments and staying nimble, they can thrive in a global environment—a valuable mindset for any modern business.

Innovative Tax and Asset Approaches

Innovative companies are constantly finding new ways to optimize their financial structure through creative tax and asset strategies. This goes beyond simply choosing between debt and equity and involves a more holistic approach to financial management.

For example, a company might lease major equipment instead of buying it outright. This keeps a large liability off the balance sheet and can offer tax advantages. Another approach is to use retained earnings to fund growth, which avoids both the cost of debt and the dilution of equity.

Some innovative approaches include:

- Leasing Assets: Reduces upfront capital needs and can provide tax benefits.

- Using Hybrid Securities: Instruments like convertible bonds offer the features of both debt and equity.

- Strategic Tax Planning: Structuring operations across jurisdictions to legally minimize the global tax burden.

Conclusion

In summary, understanding financial structure is crucial for both business stability and growth. By grasping the key components like equity and debt capital, along with the influence of factors such as risk management and tax planning, you can create a robust foundation for your organization. Whether you're a small business owner, an expat, or part of a larger corporation, tailoring your financial structure to fit your unique circumstances will help navigate the complexities of today’s global economy. Start applying these insights today to enhance your financial strategy. If you're ready to take the next step, get a free consultation to explore how we can support your financial goals.

Frequently Asked Questions

How do invisible assets affect a company’s financial structure?

Invisible assets, like brand reputation or intellectual property, boost a company's perceived value even though they aren't on the balance sheet. This higher valuation can improve investor confidence, making it easier to secure favorable equity or debt financing, thereby strengthening the company's overall financial health and structure despite asset invisibility.

What’s the relationship between financial structure and dynastic wealth?

The financial structure for dynastic wealth is designed for long-term preservation and multi-generational growth. Instead of focusing on short-term profits, its capital structure prioritizes stability and asset protection, often using trusts and family offices to manage the ownership stake and maintain the family's financial position over decades.

Is tax-aware structuring essential for global businesses in Canada?

Yes, tax-aware structuring is essential. For global businesses in Canada, it helps manage a complex financial position by navigating different tax laws within the global system. Proper tax planning ensures compliance, minimizes tax liabilities, and ultimately frees up capital that can be reinvested into the business for growth.

Follow The Jerz Way

02

Action Plan & Document Collection

We create a tailored action plan aligned with your chosen service(s). This stage includes gathering required documents and handling essential tasks such as translations, apostilles, and genealogical research.